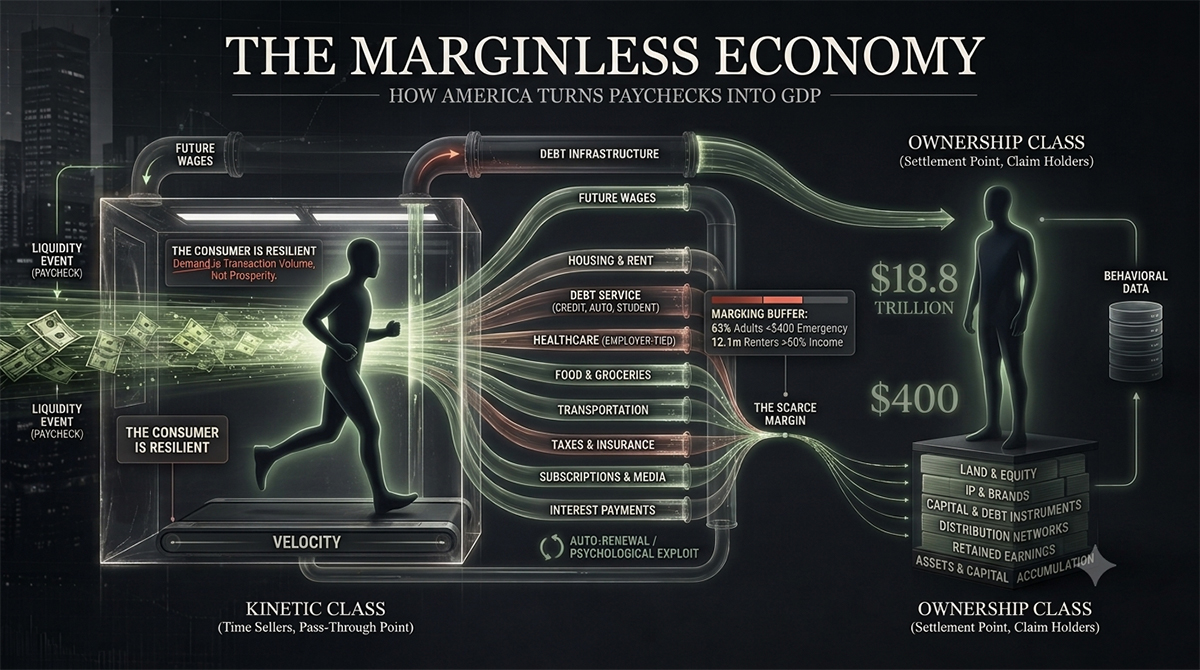

But the capture doesn’t stop there. Before the paycheck even arrives, the financial system has already borrowed against it.

Credit cards, auto loans, mortgages, student debt — these are not just products. They are infrastructure. They are pipes engineered to pull future wages into the present, charge rent on the bridge, and return a portion of tomorrow’s labor to the ownership class today. The debt economy doesn’t wait for you to accumulate money. It advances you against your future self and earns the spread.

This is why inflation hits differently depending on which side of the circuit you occupy. When prices rise, the ownership class holds assets that rise with them — real estate appreciates, equities climb, rent rolls increase. They are long on the very things that are becoming more expensive. The kinetic class gets the cost side without the asset appreciation side. Inflation is not neutral. It is structurally regressive in a way that headline CPI numbers never quite capture.

The paycheck shrinks in real terms.

The asset appreciates in nominal terms.

The gap compounds.

This does not require a conspiracy. It is more durable than that. It is arithmetic, incentives, and ownership structure.

The person who owns labor must keep selling time. The person who owns assets receives payments from time sellers. The person with no margin must comply with the next billing cycle. The person with capital can wait.

That is the real architecture of compliance.

An individual with six months of liquidity has options. An individual with two weeks of liquidity has to show up, say yes, keep moving, and hope nothing breaks.

Fragility is the parent company of compliance.

And the modern economy has found increasingly precise ways to engineer that fragility. Consider the subscription model — now the dominant revenue architecture across software, media, healthcare, fitness, and entertainment. The entire logic of recurring billing is built on a behavioral asymmetry: you must actively cancel, or the charge continues. The default is extraction. Auto-renewal is not a convenience feature. It is a psychological exploit at civilizational scale, normalized because it happens to nearly everyone simultaneously.

Then there is the attention economy operating one layer beneath all of this. Before your money can be harvested, your desire must be cultivated. Social media is not free. You pay with attention and behavioral data — data that is sold back to the companies marketing you things you did not know you needed. The loop runs like this: your behavior trains the algorithm, the algorithm amplifies desire, the desire drives spending, the spending becomes someone else’s retained earnings. The kinetic class does not merely fund the ownership class financially. They supply the raw behavioral data that makes the targeting more accurate next time.

You are not just the customer.

You are part of the product pipeline.

The modern economy does not merely reward productivity. It enforces velocity. An economy built on roughly 70% consumer spending cannot tolerate too much stillness among the people doing the spending. If too many households stop, save, refuse, downshift, or exit the cycle, the model weakens.

So the system does not need the average person to be wealthy.

It needs them liquid enough to spend, pressured enough to work, and stretched enough to keep returning to the next billing cycle.

That is the marginless economy.

Not rich versus poor in the cartoon sense. Not luxury versus struggle. The more accurate divide is between the kinetic class and the ownership class.

The kinetic class lives in motion. Their income must keep moving because it cannot sit still long enough to become capital. Money passes through them: paycheck in, bills out, debt serviced, rent paid, balance reset.

They believe they are participating in capitalism because they can choose which brand, app, subscription, car payment, apartment, or lifestyle signal to buy. But structurally, they are often a pass-through point.

There is also a subtler trap specific to the American version of this system. Employer-tied healthcare means that leaving a job — to start a business, to negotiate harder, to take a risk — carries a catastrophic downside that simply does not exist in peer economies. The cost of exit includes losing medical coverage for yourself and your family. This is not a design flaw. It is a structural feature that suppresses the labor class’s ability to leave the employment relationship. Entrepreneurship is advertised as the American path to ownership. It is also made structurally harder here than almost anywhere else in the developed world.

The kinetic class is not just economically constrained.

They are institutionally anchored.

The ownership class lives differently. Their money does not simply move. It settles. It accumulates. It buys claims on future cash flow: equity, land, debt instruments, intellectual property, software, brands, real estate, infrastructure, and distribution.

One side spends to remain functional.

The other side owns the systems that receive the spending.

That is why entrepreneurship matters, but not in the shallow motivational sense. The purpose is not to buy a nicer version of the same consumer cage. The purpose is to change your position in the economic circuit.

To move from being the pass-through point to being the settlement point.

To stop being only the customer, the borrower, the renter, the subscriber, the employee, the target demographic, the behavioral data source.

To become an owner of something that captures value after you stop actively pushing the wheel.

The great illusion is that consumption equals participation in capitalism. It does not. Consumption is access. Ownership is power.

A consumer gets choices. An owner gets claims.

A consumer chooses between brands. An owner owns the brand, the platform, the building, the debt, the data, the distribution, or the equity.

The average person is told to express identity through purchases. But identity purchased on credit is not freedom. It is a costume rented from the future.

The real game is not looking successful inside the consumption economy. The real game is building enough margin to no longer be governed by it.

Because a person with no margin is easy to control. They cannot negotiate with confidence. They cannot pause. They cannot refuse bad terms for long. They cannot take strategic risks. They must keep the income stream alive because the fixed-cost enclosure is waiting at the end of the month.

This is not merely an economic observation. There is a concept in political philosophy called structural coercion — the idea that you can be profoundly unfree not because anyone is forcing you at gunpoint, but because the architecture of your options leaves you with no viable alternative. The marginless worker technically chooses to accept bad terms. But choice under duress is not the kind of choice a free market assumes when it celebrates voluntary exchange. The system preserves the language of freedom while systematically narrowing the space in which it can actually be exercised.

This is why the economy can be statistically “strong” while people feel spiritually and financially cornered.

GDP can rise. Household debt can rise. Rent burdens can rise. Corporate earnings can rise. Subscription revenue can rise. Asset prices can rise.

And the average person can still feel like they are running faster just to remain in place.

That is not a paradox.

That is the model.

The American economy is not fragile because people stopped spending. It is fragile because it requires people with limited margin to keep spending forever.

And once you understand that, the goal becomes very clear:

Build margin. Acquire leverage. Own assets. Create income that is not entirely dependent on your immediate labor. Stop confusing consumer choice with economic freedom. Stop supplying behavioral data that makes the next extraction more precise.

The machine does not need you to be wealthy.

It needs you liquid enough to spend, pressured enough to work, and distracted enough not to notice the difference between motion and progress.

The question is not whether the economy is working.

It is working exactly as structured.

The better question is:

Are you building ownership, or are you just helping someone else’s ownership compound?